[MACRO Trends] The global crude oil market game: the complex chess game behind policy swings and strategic production increases

- 2025年7月3日

- Posted by: Macro

- Category: News

Recently, the global crude oil market has been impacted by two forces: the United States has been volatile in its policy toward Iran. Since the Trump administration withdrew from the Iran nuclear agreement and imposed strong sanctions, Iran's crude oil exports have dropped sharply from a peak of 2.5 million barrels per day in 2018 to less than 500,000 barrels; although the Biden administration has sought negotiations, it has been deadlocked due to core differences. At the same time, OPEC+ has promoted its production increase plan. Since the production cuts due to the epidemic in 2020, according to the 2023 meeting plan, it plans to increase production by about 2 million barrels per day in 2024. The combination of the two has caused WTI and Brent crude oil futures prices to fluctuate between $70 and $90 per barrel, exacerbating the geopolitical game in the Middle East and affecting the reshaping of the global energy landscape.

The US's "maximum pressure" policy on Iran is in unprecedented chaos. Recently, Trump suddenly stated on social media that "China can continue to buy Iranian oil now", which is in sharp contrast to his tough stance in May that "all Iranian oil transactions must be stopped immediately". He also bluntly stated at the NATO summit that Iran "needs funds for reconstruction" and "let them sell oil if they want to", completely ignoring the series of policies formulated by his government to strangle Iran's oil exports.

However, Trump's statement is not a policy shift. He made it clear that he would not give up sanctions on Iran, and senior White House officials also confirmed that the relevant restrictions will continue. Riboua believes that this is more likely a "calculated statement" to prevent oil prices from soaring - using market expectations to stabilize prices. Maloney, director of the Brookings Institution's foreign policy program, pointed out the core: Trump's "transactional thinking" to view the crisis has led to the current Iran sanctions policy "extremely chaotic", and this impermanence has become a new risk variable in the market.

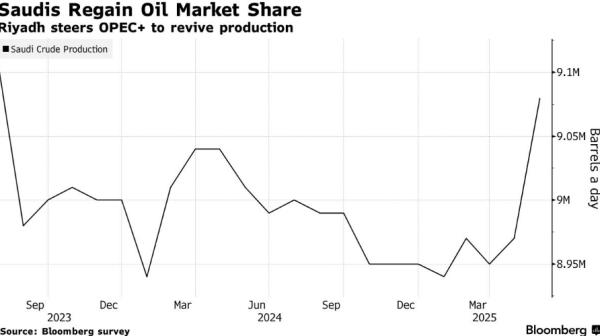

OPEC+ production increase: Saudi Arabia leads the battle for market share

In response to the swing of US policy, OPEC+ has launched a wave of production increases. Led by Saudi Arabia, OPEC+ is planning to start the fourth round of large-scale production increases this weekend, with an additional 411,000 barrels per day from August, continuing the pace of production increases from May to July. This decision stems from Saudi Arabia's urgent fight for market share - facing the erosion of competitors such as US shale oil companies, Riyadh is determined to regain the initiative by restoring production capacity.

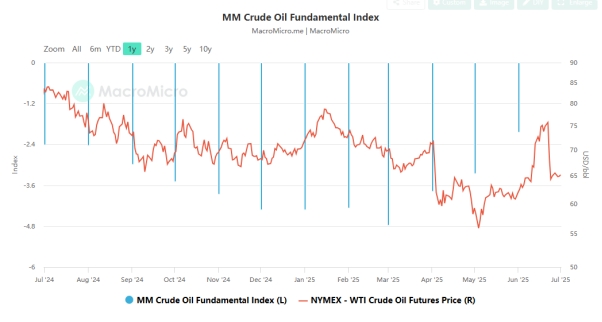

The impact of the increase in production on oil prices was immediate. Affected by this, coupled with the ceasefire agreement between Israel and Iran to ease concerns about Middle East exports, Brent crude oil futures have fallen to around $68 per barrel, down more than 9% from the beginning of the year. JPMorgan Chase predicts that oil prices may fall to just over $60 later this year and further decline in 2026. But OPEC+ seems determined. Chilingilian, head of research at Onyx Capital Group, said bluntly: "They have adopted a market share strategy, and the die is cast."

Short-term pressure and long-term layout: the future game of the global crude oil market

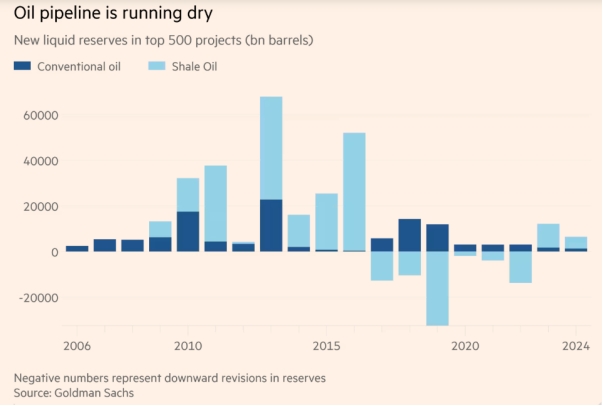

OPEC+'s logic of increasing production actually hides long-term strategic considerations. Historically, the organization believed in "reducing production to maintain prices", but behind this shift, there is not only the intention to punish overproducing member countries, but also the calculation of buffering the impact of US sanctions on Iran and giving the Trump administration a "gift of reducing inflation". More importantly, the lack of stamina of non-OPEC oil-producing countries has given OPEC confidence: Goldman Sachs data shows that the average annual discovery of non-shale oil fields in the past five years is only 2.5 billion barrels, less than a quarter of the previous three years; the US Energy Information Administration predicts that shale oil will peak in 2027 and then decline. This means that when the production capacity of competitors declines, OPEC+ is expected to regain pricing power with its inventory advantage.

In the short term, the pressure on oil prices and the intensification of fiscal pressure on oil-producing countries are inevitable: the slowdown in global economic recovery and the acceleration of new energy substitution have led to insufficient demand, and WTI crude oil futures prices have fluctuated downward by more than 15% in March; Saudi Arabia, Russia and other OPEC+ core countries have continued to rise in fiscal balance due to the growth of infrastructure and welfare spending. In the long term, the energy game has become more complicated: OPEC+'s dynamic production control and the flexible supply strategy of US shale oil are hedging, the US energy policy is swaying, and variables such as the Iran nuclear agreement and Venezuela's resumption of production have emerged frequently, continuing to reshape the global energy landscape. This crude oil game that integrates geopolitical, technological and economic interests is far from over.